This might actually be a good way to teach kids about credit and interest. Let them borrow a small amount at a high interest rate and walk them through paying it off.

It’s one thing to tell them about financial responsibility. But watching a bad choice drain their piggy bank is the sort of trauma that leaves a scar.

Let’s not scar children to teach them lessons. I’m sure there’s a better way to teach a kid about interest besides getting a loan from McDonald’s.

A couple dollars is a cheap price for such a valuable lesson.

But its just literally feeding McDonald’s for no reason . Maybe the parents could rent money to kids in this way if you really wanna teach them that " lesson" for whatever reason .

Fine, do it at In-N-Out

I finally got to try In-N-Out last week and can finally say for certain that it’s really nothing special. Might as well get a loan from Burger King.

It’s a very decent burger at a very reasonable price.

It used to be better, and the family that own the company are far right Christian extremists.

If that was the reason for it then great idea. Having to buy icecream on a payment plan is just sad and more than a little crazy

Oh I don’t know if that was the reason for the one in the image. I agree with you that needing to finance ice cream is sad. I’m just thinking it could be a good intro to predatory finance for kids.

Why even use credit at all? What is wrong with debit?

It’s for people who don’t have enough in their bank account.

Although if you don’t have $8, maybe rethink that shitty fast food.

It’s also good for safety.

Getting your credit card stolen and emptied? That’s your creditors problem (generally speaking).

Getting your debit card stolen and emptied? That’s your problem.

I use my credit cards for everything I purchase because I get some cash back or other incentives along with fraud protections.

My brother’s a psychopath who plays his credit score like it’s a game so he has like ten cards and a 800+ score he’s proud of.

I make nearly three times as much as him and it took me forever to get an 800 so maybe he’s onto something but fuck that game.

While you were at parties, I studied the FICO.

Under my tutalage, I have elevated my husband into the ranks of the >800.

I just use credit for everything and hover in the 820s. Unless there’s some substantial discount for paying cash I just don’t see the point these days.

That being said, my wonderful credit score ain’t doing shit for me. It’s not like I get some magical super low interest rate. Maybe when things calm down it’ll be worth it, but then there will be some other reason not to borrow money.

There are some nice perks to good credit outside of interest. It can qualify you for better housing, better perks on certain rentals, not having to worry about emergency situations killing your savings outright, and let’s you take advantage of stuff like cash back and bulk purchasing discounts. An example is staple foods, being able to hit the once-a-year bulk deals on stuff like rice or Lawreys garlic salt can cut the price of those items in half or better (personal examples, but the thought should hold). Ancillary perks, but they do add up.

I believe when you get serious about the tactics it’s called churning and manufactured spending

“Credit Score” exists purely to sell you more credit score. It’s only there because they were forced to let you see your own credit history, and they figured “why not monetise that somehow”, so now you’ll be bombarded with ads for more credit and loans, which boosts your “score” while giving them a sliver in affiliate fees.

Actual lenders will examine your credit history, and apply their own score. The criteria for a phone contract, am unsecured bank loan, a mortgage, etc, will all have wildly different requirements. I have one credit card that I pay off each month, and that was enough to get a house.

Paying what you owe reliably is all they’re really looking for.

Credit cards come with fraud protection and help you build a credit score, which will get you a lower interest rate on a loan, if you need one. So long as you only spend money you have on hand, and pay off your card every month in full, there’s no down side.

is this a universal thing or are you just assuming that the entire world works like the US? Here in sweden i have never heard of anyone actually using a credit card.

Yeah great point, the US has a very high emphasis on debt, for horrible reasons.

The debt industry makes so much god damned money for the companies involved in it, it’s not even funny.

Between student loans and credit cards, US citizens have a collective $1.73 trillion in debt. And let’s just assume 15% interest on average (probably a low-ball to be honest): that’s $173 billion going to these companies in interest payments per year.

Shit won’t change here because too many people with too much power are making too much money.

Why even use debit at all? What is wrong with bank notes?

Why even use bank notes at all? What is wrong with precious metals?

Why even use precious metals at all? What is wrong with big stick?

deleted by creator

Eh, valuable lessons generally are valuable because they cost you something to learn.

Anything that’s free we tend to not appreciate very much.

deleted by creator

You could just ask easily be the bank yourself and save the “interest” for a birthday gift or something later on. This really isn’t a difficult concept to use as a teaching opportunity without just screwing over a kid. Do you teach your kids to not walk into traffic by letting them get hit by a car too?

At least it should be paid off by now

Micro-financing is a concept that should be violently uninvented.

Payments Processing is its own niche highly lucrative industry. And options to convince people to finance every fucking thing are largely just rent-seeking schemes intent on nickel-and-diming the transactions of the poorest people.

I looked into using this type of service to pay for a modest purchase. A luxury of sorts. Something I had the cash for, but felt weird about paying all $600 or so for. I thought, maybe an interest free loan would be cool?

So i start to pay for the thing with klarna or whatever. And I see it’s only a six week loan. Wait, my credit card is a free six week loan (give or take). Wtf. I’d have to pay the thing off faster than just using a credit card.

I talked myself out of buying whatever it was.

I’ve used similar services to this in the past; not because I couldn’t afford something up front - but because I wanted to amortise the purchase across a pretty short (8 week) period.

Why not just use a credit card? I did. As a semi-regular user of the service, it was set up in such a way that it would bill the first 25% of my purchase after 2 weeks, and again every 2 weeks after that.

So not only was I getting an additional interest-free time stacking the 2 week period with my CC’s billing cycle; but I was earning loyalty/rewards points with both programs simultaneously.

Six weeks seems very short, all the services I’ve seen are three payments over three months.

PayPal pay in 4 is 6 weeks. It splits into 4 payments, 1 due now, 1 after 2 weeks, one after 4 weeks and one after 6 weeks

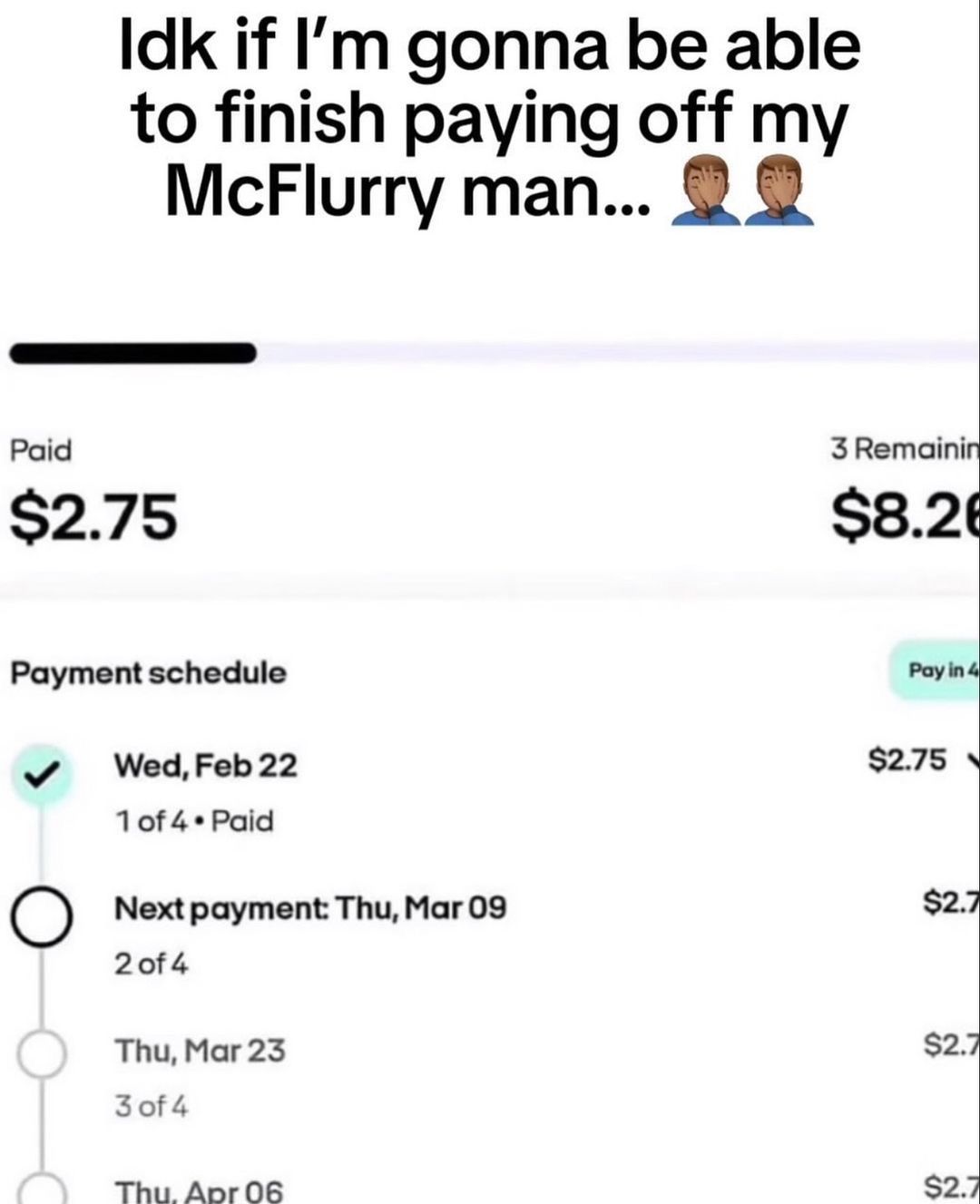

$8 for a McFlurry sounds absurd

11$ in total

What’s more absurd is that there are people willing to pay that.

What’s even more absurd is that there are people willing to finance that

I agree but let’s be real the he real absurdity here is that the ice cream machine wasn’t kneecapped by it’s own manufacturer …

A lot of our financial fuckery is due to the fact that we have so many financially illiterate people, that companies can impose bullshit like this and get away with it. So in the end we all suffer because we can’t put financial pressure against said companies since they can wait us out, surviving on the stupid.

This applies to a lot of stuff, from streaming to the to fast food to groceries.

Most of the time, these come with zero interest. I’m not sure where the money is for the companies doing these finance options, but if someone did this for a joke, it’s not that big a deal.

these come with zero interest

$8 McFlurry likely has the financing baked into the price of the product.

You’ll occasionally see businesses (SPEC’s is the local shop that leaps to mind) that will give you a discount for using a debt card rather than a credit card. That’s because the credit card company tends to charge a 2-4% transaction fee on the purchase. SPEC’s can save money by offering to discount their merchandise by some portion of that transaction fee.

The reverse is also true. A retailer that works with Klarda or some other DeFi platform can simply raise the price of all its products to cover the (typically much higher) transaction cost.

This defers the credit risk (if there’s a 12% surcharge, you don’t mind when 10% of the bills go unpaid) in a system that is highly punitive for debtors and tax-favorable to creditors.

German supermarkets tend to read your bank code from your debit card and on your second visit print you a direct debit mandate form with the receipt printer, because that’s cheaper than anything else, although a higher risk.

Credit seems like a tax on the poor.

Actually, it’s a tax on the impatient.

It’s not just impatience, for companies is usually more bet. They bet that they can earn a surplus higher than the interest rate when they invest that money now and not later.

It can be both

Poor people are often impatient.

Impatient people are often poor.

poor people generally can’t afford to wait

You don’t have to use credit, taxes are taken from you by force. Not comparable imo.

Not technically correct. If you want to be able to rent apartments or dream of owning a house, you will have to use credit in the U.S., or you’ll at least need someone with a high credit score willing to be your co-signer.

obv nobody is forcing you to get a credit card and rack up a lot of debt, but you will face a lot of struggles in life that someone who makes regular payments on a credit card will not.

That seems crazy to me. I understand that what you are saying is reality, but is it really that difficult to get by in US without ever owning a credit card?

Yes. Adding to the other comment, if you don’t have good credit you can also lose out on certain job opportunities.

Edit: here is California’s restrictions on employer access. Note that other states have fewer restrictions.

Yes. Effectively you will not have any credit history, so you simply won’t qualify for lower interest credit products or will be rejected on applications that have a credit score threshold.

You’ll be rejected from a lot of things on the basis of having no credit, because in the U.S., it is considered worse if you have always paid everything up front and on time than if you consistently borrow and make continual payments. Now, that doesn’t have to be a credit card per say, it can be car lease payments, student loan payments, medical debt payments, my landlord reports my rent payments, but credit cards are one of the easiest ways to build up your credit score before you say, have to spend an extra $1500 upfront for an apartment on a co-signor service because my credit score wasn’t considered high enough for an apartment I pay $500 a month for.

Do you have no rental bonds? It’s quite common here to have a rental bond up to three times the monthly rent, but you get that back at the end if there are no disputes about damages or payment default.

There doesn’t seem to be anything offered by the rental company I’m currently with, and I’ve never heard of concept before. There are security deposits, which you do typically receive at the end of the lease, but most of the ones here are non-refundable, and I did have to pay one of those as well.

Also, your credit cards are a different kind of “loan” - revolving - vs those other debts, which are installment. Having a mix of the two will improve your credit. They literally want it to be impossible to have good credit without the cards.

You also don’t have to pay taxes. Plenty of rich people don’t

The richest Americans lobbied the government aggressively to pay less taxes. They’re all skipping out on their fair share and foisting the burden on everyone with less than 100 million in the bank.

This is why we should eat the richest person each year and re-distribute their wealth.

Imagine all those greedy fucks using their vast wealth to investigate and call out the real wealth and scummy accounting of the other ultra wealthy.

They aren’t taken by force, you choose to live in a society that provides you with all sorts of services, which need to be paid for.

You are free to live in a society that doesn’t provide any road networks, fire departments, education, … but that is not where you live now. So I suggest you move instead of complaining about something necessary.

I heard Somalia doesn’t ask for any taxes.

Being able to live isn’t a choice.

Are you saying you need credit to live? Because that’s not true. Lot’s of people live that way, but it’s not necessary.

Have you ever been poor? Yes, sometimes you need credit to live. I’m still paying off debt from 2020 that I only acquired due to desperation and the threat of homelessness

It can be. Depending on the circumstances in life you are in, credit may be the only way you’re able to pay for food.

You can’t do that forever though. Eventually you’ll run out of credit and have to pay for it yourself. And by that point you’re probably getting crushed by the debt from a maxed out card, that you’d have been better off not using in the first place.

Correct. But it’s either this or literally starve. That’s why you’ve got people here saying it isn’t really a choice.

You are saying this like they are not aware… like telling a drowning person that if they don’t stop breathing water they’re gonna die. The point is that using credit in the first place isn’t always a choice. Just because it is for a lot, maybe even most people, doesn’t mean there aren’t a lot of other people for whom it isn’t.

You’re right, they should have just starved instead! So enlightened, thanks for setting us all straight!

These schemes are usually interest free.

They make their money similar to credit card fees, a small percentage from the merchant.

They shaft you if you don’t pay though, and I’m not sure if this is still the case but they never used to show up on your actual credit history. Which seems nice on paper, but is actually hugely irresponsible. All these credit trackers seem like an unfair scam to keep the poor in their place, but they are there to stop you getting into more debt than you can pay off. If left to their own devices, the lenders would cheerfully give you way more than you could ever hope to pay, and then come round and break your kneecaps when you inevitably fall behind.

{kind=link}